I got an IRS Notice of Deficiency. What should I do?

Updated April 11, 2026 by Jean Lee Scherkey, EA

One of the most important things you need to do when receiving an IRS Notice of Deficiency is not to ignore the notice, but to respond as soon as possible. While it is never good to ignore a letter from the IRS, even when our fight-or-flight instinct tells us to, some notices require greater urgency. An IRS Notice of Deficiency is one of those urgent notices.

What is a Notice of Deficiency anyway?

A Notice of Deficiency, also known as a Statutory Notice of Deficiency, Stat Notice, or 90-day letter, is the final notification a taxpayer will receive before the IRS makes its final assessment of tax due. The letter informs the taxpayer how much additional tax the IRS is proposing and why. Because of its gravity, the IRS sends the notice via certified or registered mail. Unless the taxpayer resolves the issue or petitions the Tax Court by the due date listed on the notice, the IRS will have the power to formally assess the tax due and begin collection actions. The good news (and yes, there is good news) is that this is not a bill. Instead of viewing the notice as your worst tax nightmare, think of it as an invitation to present your case as to why you do not owe the proposed tax before the IRS makes its final assessment. Remember, unlike other invitations, this one should not be viewed as optional. You need to respond to this “invitation.”

When does the IRS issue a Notice of Deficiency?

Usually, a Notice of Deficiency is issued when the IRS and a taxpayer cannot come to an agreement on what adjustment, if any, should be made on a taxpayer’s return during an audit or examination. This notice can be issued even if the case has already gone through IRS Appeals. It is not the first notice the IRS sends to a taxpayer regarding their tax issue. However, for some taxpayers, a Notice of Deficiency may be the first letter they receive or open. Prior notices can sometimes be mailed to the wrong address, especially if the taxpayer recently moved and did not notify the IRS of their new address. Also, prior notices may have been unintentionally disregarded as reminder letters or lost in the endless shuffle of junk mail.

Keep in mind that not all IRS notices give taxpayers an opportunity to protest the proposed balance due by petitioning the Tax Court. For example, math error notices do not give taxpayers an opportunity to contest the additional tax due before it is formally assessed. When it comes to protesting math error notices, taxpayers are usually given 60 days to request abatement of the assessed tax. If you would like more information about math error notices, Charla Suaste’s blog titled “IRS CP16 Letter | What to Know About the IRS CP16 Notice” is a great place to start!

Why is a Notice of Deficiency so urgent?

Ignoring a Notice of Deficiency can be detrimental to your peace of mind and pocketbook. If the tax matter listed in the notice is not timely resolved or an agreement with the IRS cannot be reached, you want to act quickly by petitioning the Tax Court. If you do not petition the Tax Court by the due date on the Notice of Deficiency, you will lose your opportunity to dispute the IRS’s position before the tax is assessed.

One of the biggest benefits to petitioning the Tax Court is that you can have your case heard in the Court without having to pay the balance due in advance. This is unique to the Tax Court. Usually, taxpayers who dispute a federal tax liability in the United States District Court or the United States Court of Federal Claims must pay the balance due in advance.

What should my first step be?

- The first thing you want to do is read the entire notice and take special note of the last date you have to file a petition with the Tax Court. By law, the IRS cannot offer additional time for taxpayers to file a petition with the Tax Court. So, mark this due date on your calendar or mobile app.

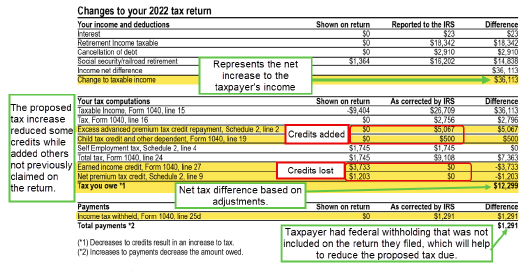

- Gather your copy of the return you filed so you can compare the information on the return with the changes the IRS is proposing to make. Usually, the proposed changes start on page 2 of the notice. Below is an image of a sample Notice of Deficiency’s “Changes to your tax return” section. The image shows the amount reported on the return you filed, the amount reported to the IRS or corrected by the IRS, and the difference between the two figures. The difference represents the proposed changes.

Let’s take a quick look at the proposed changes the IRS made to the taxpayer’s 2022 return in the image below.

- In the “Your income and deductions” section, it appears the taxpayer omitted $36,113 of income on their originally filed return, consisting of interest, retirement, cancellation of debt income, and Social Security retirement income.

- The additional income impacted the calculation of the taxpayer’s credits and total tax.

- The proposed additional income triggered an Advance Premium Tax Credit repayment of $5,067, where the taxpayer did not have an Advance Premium Tax Credit repayment calculated on their originally filed return.

- It appears the taxpayer’s originally filed return omitted an Other Dependent tax credit of $500, which the IRS gave credit for in the proposed assessment.

- Unfortunately, it appears the taxpayer’s proposed increase in income has made them ineligible for the Earned Income Tax Credit and the Premium Tax Credit of $1,203 the taxpayer claimed on their original return.

- It appears the taxpayer omitted federal income tax withholding that was reported to the IRS by a third party on their originally filed return. It is possible the withholding could have come from the additional retirement income reported by a third party to the IRS. The withholding will help reduce the total tax liability the IRS is proposing.

One of the most common reasons why the IRS issues a Notice of Deficiency is that income that was reported to them by a third party, like an employer, bank, or other financial institution, was not included on the taxpayer’s submitted return, or they cannot determine where/if the income was included. For example, if the notice includes income from a Form 1099-K or 1099-NEC, and the taxpayer has a business Schedule C included in their return, the IRS may not be able to determine if the amount reported by the third party is included in the gross receipts or sales on Schedule C.

What should I do if I agree with the notice?

If it looks like the notice is correct and you inadvertently omitted income on your return, entered the amount incorrectly, or perhaps added an unintentional “0” to the end of a number you entered, such as your mortgage interest deduction, you will want to let the IRS know you agree with the proposed assessment. You do this by signing, dating, and returning the included Form 5564, Notice of Deficiency - Waiver. The most direct way to submit your signed Form 5564 is by scanning the QR code on the notice or logging onto the IRS’s Document Upload Tool at IRS.gov/DUTReply. Your notice will include an access code that you will need when accessing the IRS’s Document Upload Tool. You can also mail your complete Form 5564 to the address listed on the notice. Even though you agree with the proposed adjustments, it is important to respond and submit the completed Form 5564. This lets the IRS know you received the notice and are proactively replying. This may help any future correspondence with the IRS go more smoothly.

What if I owe additional tax?

Don’t forget about your payment. While payments cannot be made through the Document Upload Tool, they can be made online, with a few options available. For more information on how you can make your payment, please review the IRS’s “Make a payment” webpage. While it is generally safer and easier to make your payment electronically, the IRS is still accepting paper checks (for now). On March 25, 2025, the President signed Executive Order 14247, which phases out the IRS's issuance and receipt of paper checks. If you decide to send a paper check by mail, be sure to confirm with the IRS that they still accept payments by mail. As with all correspondence sent to the IRS by mail, it is best to send it certified with a return receipt requested.

Since the tax was supposed to be paid by the due date of the return, usually April 15th, interest will be added to the balance due. Generally, interest cannot be reduced or removed as it is required to be charged by law. Once the IRS receives the completed form, they will send you a bill for the additional tax due, including interest and possibly a penalty or two. Happily, certain penalties can be waived. For more information on reducing or removing penalties, please click here. If you are unable to pay the balance due, the IRS offers various payment options. To review these options, please click here.

A word of caution

If you only partially agree with the notice, do not fill out Form 5564. This form should be completed and submitted only when the taxpayer fully agrees with the additional tax due.

What should I do if I partially or completely disagree with the notice?

What happens if you partially or completely disagree with the proposed additional tax due? The IRS gives taxpayers 90 days (150 days if they live outside the U.S.) to resolve the matter.

If you have between 60 and 90 days before the 90-day period ends, you may want to submit a statement to the IRS explaining why you disagree with the notice. You can still submit your statement anytime between the day you receive the notice and the last day to petition the Tax Court. However, the sooner you send your statement disagreeing with the assessment, the better. Due to extensive DOGE cuts to IRS personnel and the time required to respond to correspondence, it can take several weeks to months for the IRS to respond.

Include any documentation that supports your position with your response. Your statement and additional documents can be submitted electronically through the IRS’s Document Upload Tool. Your notice will include the access code you need to use when accessing the IRS Document Upload Tool. You can also submit your statement and documents by mail, but remember that your time is limited, so responding online may be the most efficient. Remember, if mailing, it is best to send it certified with a return receipt requested.

What if I am running up to the petition filing deadline? Should I delay filing my petition with the Tax Court if I have already submitted a response and am waiting for the IRS’s reply?

If you have not been able to resolve the matter with the IRS and the 90-day window is close to expiring, you will want to submit a petition to the Tax Court. Petitions can be filed by mail, in person at the clerk's office of the Tax Court, or through the Court’s online portal, DAWSON. It is important that you do not submit your petition to the IRS. Petitions must be filed with the U.S. Tax Court. A non-refundable $60 fee must be submitted with the petition. However, the fee may be waived if you are unable to pay. To see if you qualify for the Waiver of Filing Fee, please click here.

Once your timely petition is received, the Tax Court will issue you a Notice of Receipt of Petition and a docket number. If you file your Tax Court petition online, you should automatically receive a docket number. The Notice of Receipt of Petition will be sent to you electronically within the next day or two.

While you are waiting for your day in Tax Court, you will have the opportunity to resolve the matter through the pre-trial Appeals process. If you are concerned about the amount of interest accruing on the proposed balance due, you can post a bond called a “6603 Deposit.” To learn more about bond payments, please review “Bond Payments to the IRS | What You Should Know.” It is important to write the check out to the “U.S. Treasury” and to designate the payment as a “6603 Deposit.” Any payments without this designation will be interpreted as an agreement with the proposed assessment.

Keep in mind that there are no extensions to the 90-day window. The Tax Court petition deadline is taken very seriously. In fact, even if you are mere seconds late, your petition will be considered untimely and denied. When submitting your petition online through DAWSON, be sure to file it by 11:59 p.m. Eastern time on the due date. Even if you live in a different time zone, you must file your petition with Eastern time in mind. One taxpayer learned this the hard way when they filed their petition 11 seconds too late.1 The taxpayer appealed the denial of the petition to the Tax Court, which ruled that the petition was untimely. Whether filing electronically, in person, or by mail, be sure to allow yourself at least a week’s worth of “wiggle room” in case the unexpected happens. While taxpayers are given an additional 14 days (plus any days lost due to inaccessibility) to file a U.S. Tax Court petition if the filing location is unavailable, the situations that qualify are limited. The filing location must be “inaccessible or otherwise unavailable.” In the case of a taxpayer filing their petition online using DAWSON, inaccessible or unavailable means the site was down and non-operational. A taxpayer having computer or internet issues on their end does not mean the system is inaccessible or unavailable.

What happens if I miss the window to file a Tax Court petition?

If the 90-day window passes without resolving the issue or filing a petition with the Tax Court, the IRS will assess the tax, send a bill to the taxpayer, and start the collection process. Fear not, for all is not lost! In addition to possibly filing an appeal through the IRS Appeals Office, you can:

- Request an Audit Reconsideration,

- Pay the amount of tax due and then file a formal claim for refund by submitting a Form 1040X, Amended U.S. Individual Income Tax Return, or

- Pay the balance due and then file a suit for refund in the United States District Court or United States Court of Federal Claims.

- File an Offer in Compromise based on Doubt as to Liability, but keep in mind that this option is limited to only certain circumstances.

Receiving a notice from the IRS is never fun and, in fact, it can be scarier than a room full of laughing clowns in a fun house. The worst thing you can do is freeze and do nothing. By being proactive, you ensure you only pay what’s rightfully due.

[1] Sanders v. Commissioner, 160 T.C. No. 16, June 20, 2023

Do you owe money to the IRS or State?

Jean Lee Scherkey, EA

Tax Content Developer