What is the Qualified Business Income Deduction (QBID)?

July 15, 2026 by Veselina Arangelova, EA

Qualified Business Income Deduction Explained: What Changed After the Big Beautiful Bill Act of 2025?

If you currently own or are considering owning a small business, freelancing, or earning income outside of a traditional W‑2 job, there’s a powerful tax break you may have heard about but not fully understood: the Qualified Business Income Deduction (QBID), also called the Section 199A deduction because that’s where it lives in the Internal Revenue Code.

This deduction has helped many business owners lower their taxable income since it was introduced by the Tax Cuts and Jobs Act of 2017. For years, it also raised an important question: Is it just a temporary measure and will it expire? The One Big Beautiful Bill Act of 2025, also referred to as OBBBA, or BBB, is part of the reason this topic is back in the spotlight. This recent legislation made the deduction permanent and available to more business owners than ever before. Let us dive into it.

This blog post is part of our “before vs. after OBBBA” series and is the perfect opportunity to cover: (1) the changes introduced by the new legislation, (2) the difference between a deduction and a credit, (3) where the QBID fits on your return and why that matters, (4) what income qualifies, (5) the major limitations, and (6) what happens when your income is over the threshold amounts and you must use alternative calculations.

Before vs. After Comparison Table

The One Big Beautiful Bill Act expands the Qualified Business Income Deduction (QBID), not just making it permanent. Here is a quick side-by-side comparison before we discuss each change.

| Feature | Before OBBBA | After OBBBA |

| Is the QBID permanent? | Scheduled to expire after 2025 under prior law. | Made it permanent with no expiration date. |

| Maximum deduction | Up to 20% of QBI (subject to limits). | Still up to 20% of QBI, but the limits have increased. |

| Itemize required? | No, available whether you take standard or itemized deduction. | No change; it is still the same. |

| Above-threshold complexity | W‑2 wage/property limits and SSTB rules phase in. | Same framework, but with wider phase-in ranges. |

| New minimum deduction concept | Not available under prior law. | A minimum deduction allowed for certain active businesses. |

There are three areas where the current law differs from previous law: there is no set date for this deduction to expire and not be available for taxpayers, the income limits are now higher which makes more people eligible for the deduction, and there is a new minimum deduction allowed for certain businesses which was not available until now.

Deduction vs. Credit: What is the Difference?

Often the word “deduction” is used in everyday conversations taxpayers have with friends and family to describe expenses turned into benefits come tax time – but a tax deduction and a tax credit work in quite separate ways and should never be mistaken for being the same.

A legitimate tax deduction reduces the amount of income that is subject to tax. If you have $100,000 income and a $10,000 deduction, you are taxed as if you earned $90,000.

A tax credit, however, reduces your tax bill, dollar for dollar, after your tax liability is calculated. If you owe $5,000 in taxes and qualify for $1,000 credit, your bill becomes $4,000.

Both deductions and credits impact a taxpayer’s return, and in very few circumstances you must choose one or the other (like the foreign tax credit, but this is not the topic of our blog today). The Qualified Business Income Deduction is a deduction, as the name clearly states, and not a credit, so it reduces taxable income rather than directly cutting your tax bill by a fixed amount.

How does it work?

The QBID allows certain owners of pass‑through businesses to deduct up to 20% of their qualified business income when calculating federal taxable income. A qualified business income is calculated as ordinary business income minus ordinary business expenses. Pass-through businesses include many sole proprietorships, partnerships, S corporations, and certain trusts and estates. As a reminder, a pass-through business is one where all income and expenses flow through to the owner of the business to report and pay tax on the profits. Because the owner is responsible for the reporting, the business itself typically does not claim the deduction—owners claim it on their personal return. It is important to clarify that, when calculating the deduction any income earned as an employee (W-2 wages), guaranteed income and income earned through a C corporation must be excluded.

To illustrate, think of this simple example: Betty is a sole-proprietor and sells custom greeting cards online. She earns $15,000 from online sales and has $5000 of ordinary business expenses. Her qualified business income for the QBID is then $10,000, and she can deduct $2,000 on her return as a business deduction. The calculation is $10,000 * 0.20 = $2,000 of QBID.

Now, you might say “This is a very straightforward example and calculation!” and that is okay. It is only meant to help with your understanding of the mechanics of this deduction. There are many businesses for which this deduction calculation will be a bit more involved, but for the most part it is exactly how it goes for the majority. Before we dive into the situations that can complicate this calculation, let us answer one more major question: Where does the QBID fit on your tax return, and why is it so powerful?

One reason the QBID is so valuable to business owners is because it shows up on the return. The QBID is taken after you have adjusted your income and subtracted either the standard deduction or the itemized deduction. That means you benefit from both deductions, and it is not a requirement that you itemize to get the QBID.

What Income Qualifies for the QBID?

In plain terms, qualified business income is generally the net profit from operating an eligible U.S. trade or business. Common examples include:

- Net profit from a sole proprietorship (often shown on Schedule C)

- Your share of income from a partnership

- Your share of income from an S corporation

- Certain income from trusts and estates

The QBID separately addresses income received from qualified Real Estate Investment Trust (REIT) and qualified publicly traded partnership (PTP) income.

Income that does not qualify includes wages earned as an employee, guaranteed payments, most investment income (such as capital gains and dividends), and income from C corporations.

What is the new minimum deduction?

This is the most exciting expansion of this code section, second to making the deduction permanent for business owners and freelancers. Under the new law, if you have at least $1,000 of qualified business income from all active trades or businesses, then you can take a $400 deduction on your return, instead of the $200 that might be allowed if we strictly follow the 20% rule. This is meant to help those who are just getting started. This guaranteed deduction, if you will, is inflation adjusted, so it will change from year to year. What you need to remember is that you will always take the greater of the 20% or the inflation-adjusted amount.

Key Limitations You Need to Know: What is the “Lesser of” Rule?

Even if you have qualified business income, the deduction is limited. One major cap is that your total QBID cannot exceed 20% of your taxable income (before you take the QBID) minus your net capital gains. This matters because it is possible to have business income but a lower taxable income after deductions, especially if you also have capital gains or other items that affect the limit. Let us go back to Betty, our business owner, and look at another example to illustrate this rule.

Making custom greeting cards is not Betty’s only income. She has a day job as a writer and earns $50,000. After taking the standard deduction, which for 2025 is $15,750 as a single person, her taxable income before the QBID is $50,000 - $15,750 = $34,250. To calculate the limitation, we multiply her taxable income by 20% and find that the maximum for Betty to take is $6,850. Based on what we know about her business income and expenses, we previously calculated her deduction to be $2,000, so the lesser of the two amounts is reported on the return.

There may be a time when our business owner, Betty, sells so many greeting cards that the qualified business income is more than what she makes as a writer, and her deduction may exceed that deduction ceiling. That may very well be the case for you and your business. What you need to remember is that in such instances you take the lesser of the two amounts, and that becomes your deduction.

More Limitations: The Curious Case of Income Thresholds

Can the QBID get more complicated? The simple answer is yes, it sure can. As mentioned before, calculating the QBID is simplest when your taxable income is below a certain threshold amount.

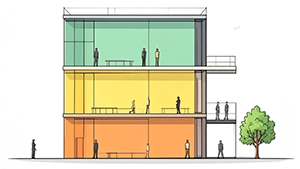

I would like you to think of these thresholds as a three-story building and it matters on which floor you currently reside. For tax year 2025, our first, second and third floor residents are grouped as follows:

I would like you to think of these thresholds as a three-story building and it matters on which floor you currently reside. For tax year 2025, our first, second and third floor residents are grouped as follows:

- First floor: Single filers earning up to $197,300 and married joint filers earning up to $394,600.

- Second floor: Single filers earning more than $197,300 but below $247,300 and joint filers earning between $394,600 but below $494,600.

- Third floor: single filers earning above $247,300 and joint filers earning above $494,600.

You should know, these numbers will change year-to-year based on an inflation adjustment, but the principle remains the same. Those who are currently first floor residents can often take a straightforward 20% deduction on qualified business income. The upper floor residents will need to get a bit more involved to determine how much they can deduct their returns because the QBID may be limited by W‑2 wages, qualified property, and—if applicable—specified service business rules. If you are currently moving in on that second floor, you may get a partial deduction. If you are a third-floor resident, then limits can apply, and there may not be a deduction at all.

Specified Service Trades or Businesses (SSTBs)

Businesses are treated differently once income exceeds the threshold amounts, and the income is derived from a specific service. Examples can include fields such as law, health, accounting, consulting, and financial services. These are called specified service trades or businesses (SSTBs).

Back to our three-story house full of residents. If your next-door neighbor is a lawyer and he lives on the first floor, then generally he can qualify like other businesses for the full 20% deduction. If he is a second-floor resident, the deduction can be reduced. If he is a third-floor resident, however, the deduction can be further limited.

There is no requirement that you memorize how the QBID is calculated in exceptional cases where there is a lot of income, so we will not get into that calculation. The key here is that once you are above the threshold, payroll and business assets can affect how much QBID you can claim, sometimes reducing the deduction below the simple 20% calculation.

Because legislation constantly evolves, you must always rely on official IRS guidance and current-year forms and instructions when applying the rules to a real return. If you are not sure how to proceed or if you have a complicated return, even multiple businesses, consult a tax professional.